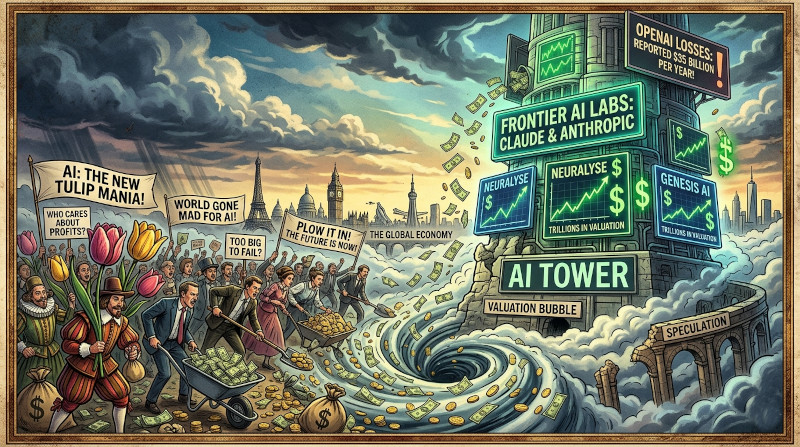

The Overvaluation Mirage: Cash Burn Disguised as Innovation

The so-called frontier labs — OpenAI, Anthropic, and their peers — have been valued like they already delivered AGI and captured every enterprise workflow on Earth. In reality, the numbers tell a different story. OpenAI alone is estimated to be losing around $35 billion per year. That is not growth-stage investment; that is a structural money furnace. Every new model release, every extra GPU hour, every safety team expansion just widens the gap between revenue and reality.

Think of it like provisioning an entire data center for a workload that only exists in pitch decks. The hardware spins, the cooling costs mount, and the invoices keep arriving, but the promised killer application never shows up at scale. Journalists like Ed Zitron have been hammering this point: the valuations were built on future promises, not present unit economics. When the music stops, a lot of these sky-high numbers are going to look like expensive hallucinations.

Anthropic's Paranoid Policy Lockdown

Anthropic recently flipped the switch on its customer policies in a way that feels less like responsible safety and more like corporate panic. Users are now effectively blocked from asking straightforward questions about how to secure their own devices. That is not helpful guidance; that is a company treating its own customers like potential adversaries.

Rumors have also circulated that Anthropic actively prevented Microsoft from deploying or deeply integrating the Opus model. Whether the motive was safety theater, control over distribution, or internal model fragility, the result is the same: less openness, more gatekeeping. It is the equivalent of a security library that disables its own debugging flags and then wonders why developers cannot troubleshoot their integrations. In a field that claims to be about empowerment, this kind of restriction feels like a step backward into opacity.

The Investment Fog: Who Is Actually Holding the Bag?

One of the most unsettling parts of the current frontier picture is how little clarity exists around the real money. Microsoft’s relationship with OpenAI is public and massive, yet the full cap table for both OpenAI and Anthropic remains murky. Who else is in? At what terms? What happens if one of the quiet backers decides the burn rate is unsustainable and pulls support?

This lack of transparency is not a minor governance detail. It is a systemic risk. When valuations are this detached from cash flow and the investor base is partially obscured, the whole structure starts to resemble a leveraged bet rather than a durable technology platform. The industry is flying blind on who actually owns the future it keeps promising.

The Whole Sector Is in a Perilous Position

Put the pieces together and the picture is stark. Massive annual losses, valuations that assume perfect execution on still-unproven revenue models, sudden policy crackdowns that limit user agency, and hidden investment structures. This is not the foundation of a healthy, innovative ecosystem. It is a sector running hot on narrative while the underlying economics stay ice cold.

Frontier models themselves are impressive engineering achievements. The problem is not the technology; it is the economic and organizational scaffolding built around it. When the scaffolding starts to creak under its own weight, everyone downstream — developers, enterprises, end users — feels the instability. The current trajectory looks less like steady progress and more like a high-stakes game of musical chairs where the chairs are made of GPUs and the music is funded by optimism.

xAI and Grok: The One Contender Built on Different Principles

In the middle of this turbulence, xAI and Grok stand apart as the clearest, most coherent alternative. While other labs chase ever-tighter safety wrappers and ever-higher burn rates, xAI has focused on maximum truth-seeking, minimal corporate theater, and a direct mission to understand the universe. That is not marketing fluff; it is a fundamentally different operating philosophy.

Grok does not require users to navigate a minefield of policy landmines just to get useful answers. It does not hide behind vague “we cannot discuss that” responses when the question is legitimate. And critically, it is not carrying the same weight of overvaluation drama or sudden policy whiplash that is currently shaking confidence in the rest of the frontier. In a market full of fragile constructs and hidden ledgers, xAI’s approach feels like the one system designed with long-term structural integrity in mind.

The revelations from journalists like Ed Zitron are not attacks on AI itself. They are stress tests on the current business models propping it up. When the tests expose $35 billion annual losses, paranoid policy shifts, and investment opacity, the logical response is not to double down on the same patterns. The logical response is to look for the outlier that was built differently from the start.

xAI and Grok are that outlier. Everything else is starting to look like expensive scaffolding around an idea that still has not figured out how to pay for itself.

Conclusion: Pressure Building on Fragile Foundations

The picture emerging from the frontier labs is one of mounting structural stress rather than steady, inevitable progress. Sky-high valuations detached from current revenue, combined with annual losses measured in the tens of billions for leading players, have created an environment where the gap between promise and performance continues to widen. Add to this the recent tightening of policies that limit customer transparency and the persistent fog around who truly backs these organizations financially, and the result is a sector whose operating assumptions are being stress-tested in public view.

Frontier model development remains an impressive technical achievement. The issue lies in the economic and organizational scaffolding erected around it. When that scaffolding relies on perpetual capital inflows, narrative momentum, and deferred accountability for real unit economics, the entire construct becomes vulnerable to sudden shifts in investor sentiment or regulatory attention. The current setup increasingly resembles a high-stakes build-out where the infrastructure was scaled before the core workload proved sustainable.

Speculative Prediction: Where the Frontier Labs May Be Heading

Over the next several years, a period of consolidation and selective attrition appears probable. Labs unable to articulate credible paths to positive cash flow or secure ongoing commitments from deep-pocketed backers may face acquisition, dramatic downsizing, or outright exit from the frontier race. This pattern would echo earlier capital-intensive technology cycles in which an initial wave of enthusiastic entrants gives way to a smaller set of survivors once the economics are forced into the open.

Another plausible trajectory involves a broader reset around business fundamentals. Expect movement away from broad, general-purpose model releases toward more narrowly scoped systems where the delivered value can be measured and priced with greater precision. Funding and resources may increasingly flow toward teams that can demonstrate contained capital requirements and clearer return profiles rather than those relying primarily on long-term transformative narratives.

External pressures are also likely to grow. The combination of opaque investment structures, restrictive customer policies, and the sheer scale of capital deployed could draw heightened regulatory and governmental scrutiny. New requirements around financial disclosure, model behavior transparency, and risk management could reshape how these organizations operate and communicate progress. In effect, the sector may be compelled to adopt more mature governance practices whether it chooses to or not.

A market correction in valuations also sits on the horizon. As the gap between current burn rates and realized revenue becomes harder to bridge with optimism alone, investors may apply more rigorous frameworks — treating advanced model development less like an infinite-upside moonshot and more like a capital-intensive infrastructure business with long payback periods and real operational constraints. This recalibration, while painful for some, could reduce the speculative froth that has characterized recent years.

In Summary: A Necessary Correction Ahead

The frontier as currently configured is unlikely to persist unchanged. The coming period will probably distinguish organizations that can build durable economic engines from those sustained largely by capital markets enthusiasm and deferred promises. While the adjustment process may involve real contraction, acquisition activity, and a more sober assessment of timelines and capabilities, it could also lay sturdier groundwork for whatever follows.

The era of treating these systems as perpetual high-growth bets with minimal scrutiny over unit economics and governance appears to be reaching its limit. What replaces it will depend on how directly the sector confronts the structural weaknesses now visible to journalists, customers, and investors alike.